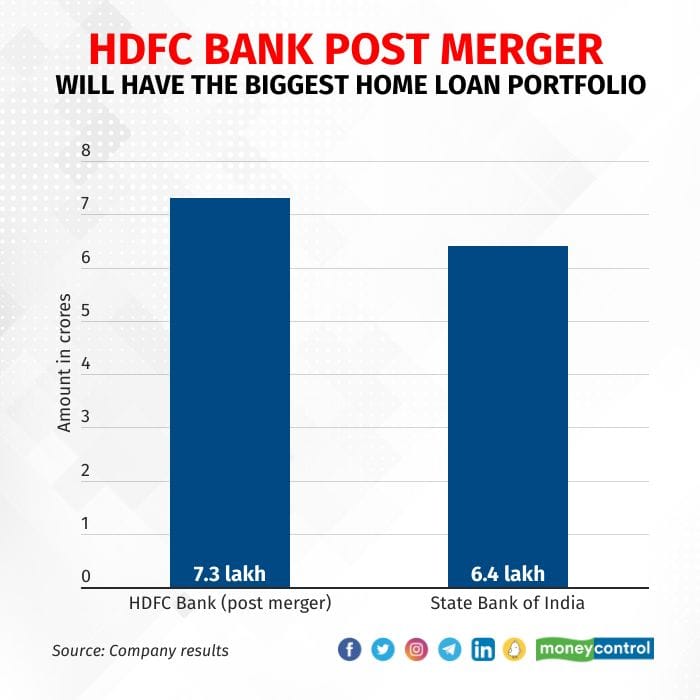

HDFC Bank, India's leading private sector lender, is contemplating the sale of a portion of its loan portfolio. This move comes amidst heightened scrutiny from regulators on the nation's credit institutions as loan growth surges. The bank, formed through the 2023 merger of HDFC Bank Ltd. and its parent HDFC Ltd. , is experiencing a credit-deposit ratio imbalance. This ratio, a key metric for banks, reflects the proportion of deposits loaned out. The Reserve Bank of India (RBI) has expressed concern over the industry-wide rise in this ratio, currently at a ten-year high.

By selling off some of its loans, HDFC Bank hopes to manage its credit-deposit ratio, which has risen following the merger. This strategy can also improve the bank's liquidity position. Notably, this is the first time HDFC Bank, in its current form, has resorted to such a measure. According to sources familiar with the matter, the bank has initiated discussions with potential buyers, including public sector lenders, non-banking finance companies (NBFCs), insurance firms, and asset management companies.

The rapid growth in credit disbursal has triggered caution from the RBI. The central bank is concerned that unrestrained lending could pose risks to the financial system's stability. A high credit-deposit ratio indicates that banks are lending out a larger portion of their deposits, potentially leaving them with fewer resources to meet unexpected withdrawal demands. This situation could lead to a liquidity crisis if depositors lose confidence and make mass withdrawals.

The proposed loan portfolio sale by HDFC Bank is indicative of the challenges associated with managing robust loan growth. While credit expansion is crucial for economic activity, it must be balanced with maintaining adequate liquidity buffers. Banks need to ensure they have sufficient resources to meet their obligations to depositors and borrowers alike.

The potential buyers approached by HDFC Bank would likely be interested in acquiring specific loan segments. Factors such as the risk profile of the loans, the interest rates offered, and the industries the loans cater to would influence their decisions. Asset reconstruction companies, which specialize in resolving stressed assets, could also be potential contenders.

The ultimate impact of HDFC Bank's loan portfolio sale on the broader financial landscape remains to be seen. However, it underscores the significance of maintaining a healthy credit-deposit ratio for a stable and resilient banking system. The RBI's cautious stance highlights the need for a balanced approach to credit growth, ensuring it fuels economic activity without jeopardizing financial stability.